Blockchain for conferences and events is not a thing yet and for good reason. Most people don’t actually understand how it works. I can’t say I blame anyone, it is not an easy thing to wrap your head around. Really. I think that I am fairly intelligent, I mean, I don’t inject bleach or eat Tide Pods so I have that going for me. Even so, It took me about four sit-downs before my brain began to understand and once it did, the implications for the meetings and events industry became apparent.

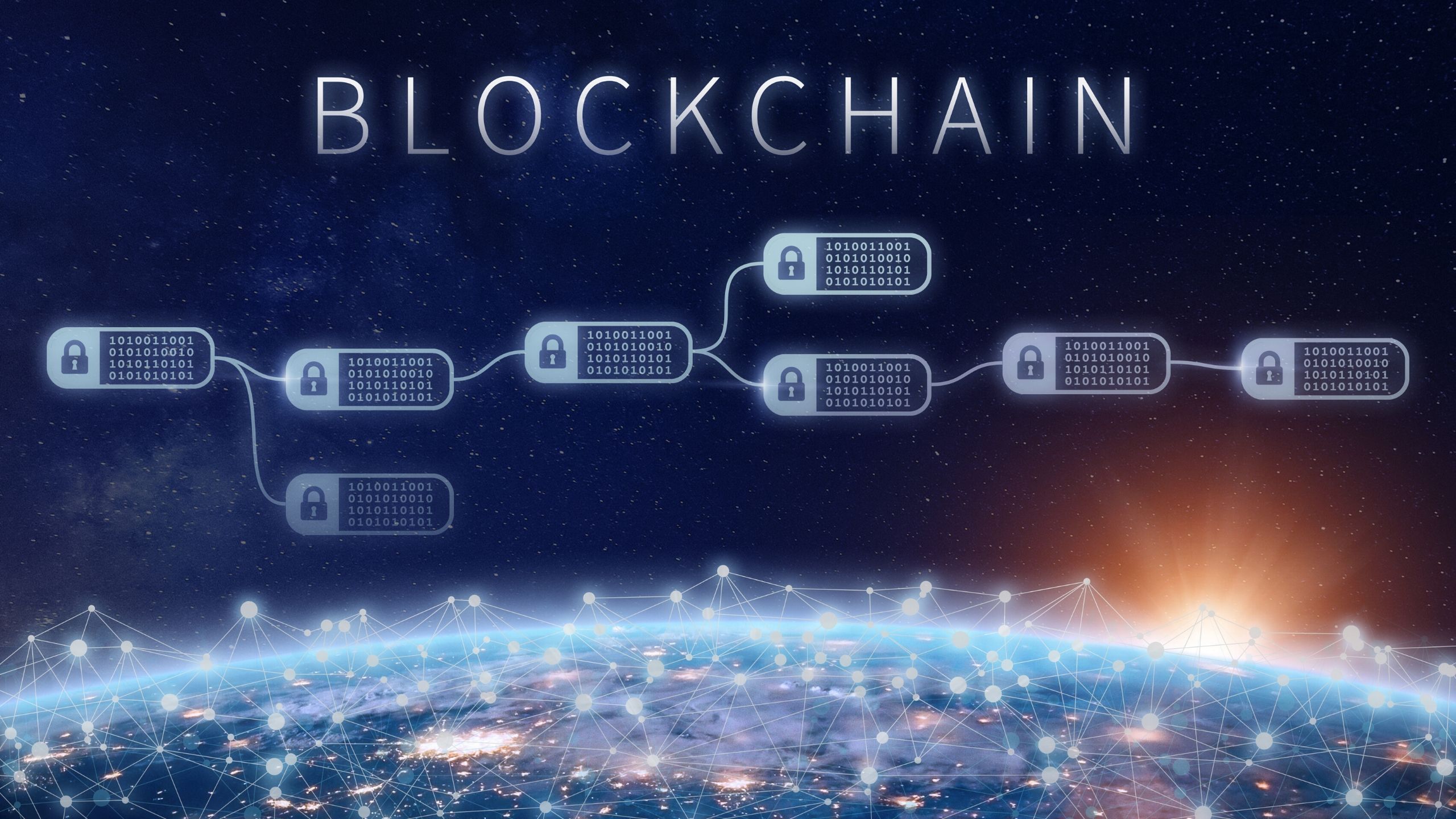

In its most basic form, the blockchain is simply a way to manage data without a central administrator by using a distributed database, a ledger. No one organization owns the data, which means that the attendee is in control rather than a government, association, or event management company. All of the data confirmations are handled by a distributed network of computers across the globe. In the case of the Cryptocurrency Bitcoin, this means that thousands of volunteer-run computers confirm and authorize each transaction by verifying that each block of information is correct. Blockchain is a near flawless way to ensure that data has not been altered or tampered with and it can’t be stolen. If one block in the chain does not match the rest, the whole transaction is invalid.

While this explanation is very simple, I hope that it sparks your interest because you are about to learn a whole lot more. Last week, we had the opportunity to sit with Tracy Leparulo, one of the world’s foremost experts on how blockchain will impact the event industry for the podcast The Event Tech Pull Up which we produce in association with isocialx.

Catch the episode below or head over the podcast website where you can subscribe with your favorite podcast app!